We all save money. It feels good to set something aside. But here is the truth: prices do not stay the same. They keep rising.

If you save INR 1,00,000 today, what will it actually buy after 10, 20, or 30 years?

And is the “official” inflation number really what you feel in your daily life

Table of Contents

(1) First, what is inflation?

Inflation means things get more expensive over time. When prices go up, your money buys less.

- A tomato costs INR 50 today.

- Next year, it might cost INR 53.

- So your INR 100 buys fewer tomatoes.

This happens with everything-school fees, hospital bills, travel, rent, groceries. That is inflation

(2) Official inflation vs your inflation

India’s official inflation (called CPI) is a national average. The RBI tries to keep it around 4%, give or take 2%. But this number is based on a general basket of goods. Your spending may be very different.

For example, if you spend more on education or healthcare-things that often get expensive faster-your personal inflation could be much higher.

That’s why even if your salary goes up with CPI, it might still feel like you’re falling behind.

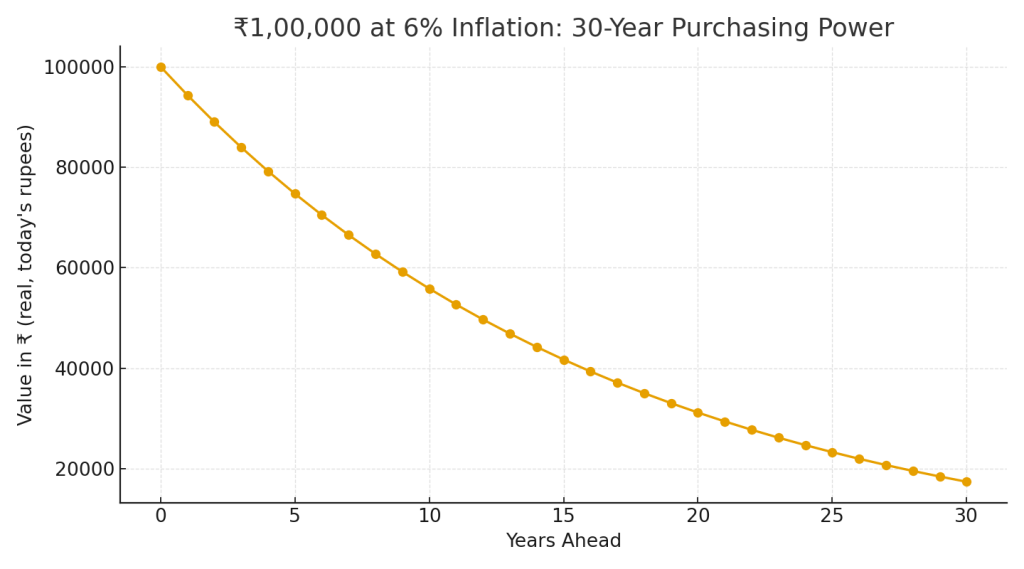

(3) What happens to INR 1,00,000 at 6% inflation?

Let’s say inflation stays at 6% every year. Here’s how your INR1 lakh loses value over time

| Year | What INR 1,00,000 Can Buy |

|---|---|

| Today | INR 1,00,000 |

| After 10 years | INR 55,800 |

| After 20 years | INR 31,400 |

| After 30 years | INR 17,400 |

So in 30 years, your INR 1 lakh will buy only what INR 17,400 buys today. That is a big drop in value.

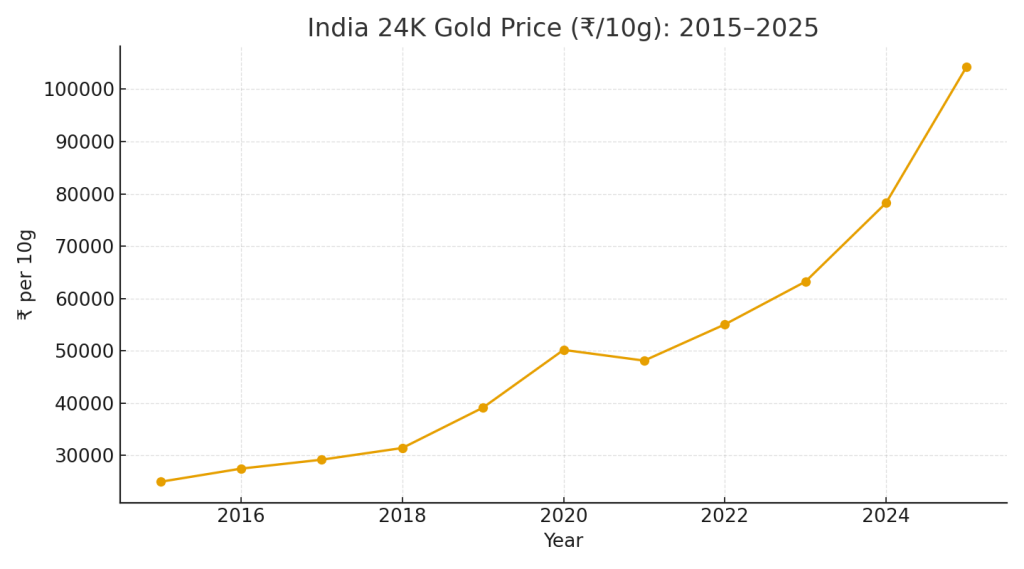

(4) What if prices rose like gold

Gold prices have gone up a lot in the last 10 years. Let’s look:

- 2015: INR 24,931 per 10g

- 2025: INR 1,04,320 per 10g

That is more than 4 times higher.

Now imagine if everything-food, rent, school fees—rose like gold.

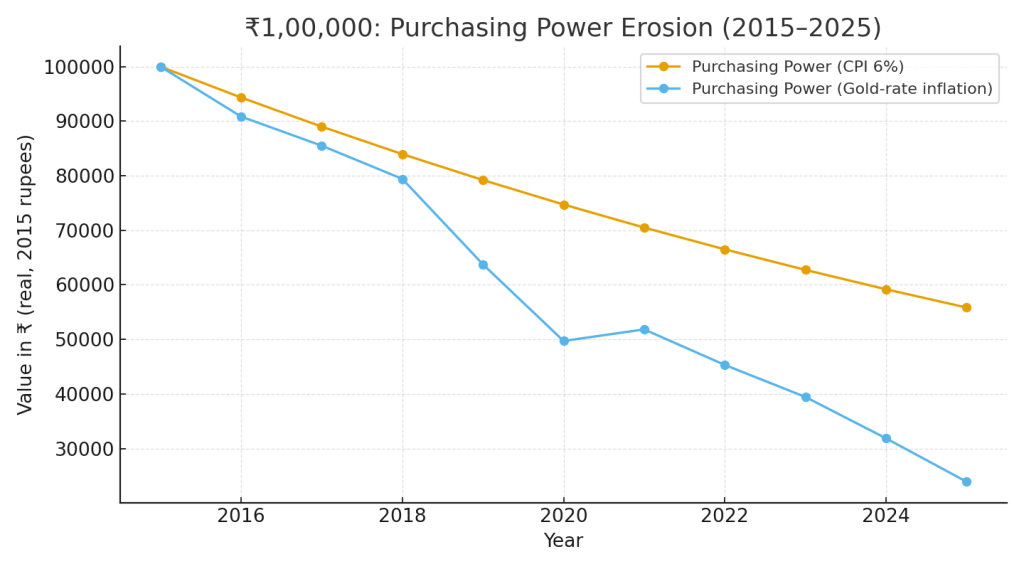

- At 6% inflation: INR 1,00,000 (2015) → INR 55,800 (2025)

- If prices rose like gold: INR 1,00,000 (2015) → INR 23,900 (2025)

That’s a huge loss in value.

(5) Purchasing Power Erosion (2015-2025)

Final thought

Inflation is slow, but powerful. It quietly eats away at your savings. If your money is not growing faster than inflation, you arre losing buying power every year. So ask yourself: Is your money just sitting, or is it growing?

Is the government “hiding” real inflation?

No. CPI is a standard, transparent measure. But it is an average. Your life = your own basket. Compare your spend with CPI and plan accordingly.

Should I plan using gold inflation?

Not as the only measure. Use it as a tough scenario. If you can meet goals even under that, you are safer.

What number should I use for planning?

For many urban families, 6–8% is a conservative planning band. If your costs are fee/health heavy, aim higher.